Another sign of the times:

The Teamsters Central States Pension Fund, which covers 400,000 participants, 220,000 of them retired, is proposing significant pension cuts. F'rinstance, a retiree presently receiving $3000-per-month may have his pension cut to less than $1200-per-month.

Some current retirees complain "“This pension should be paid out in full until it’s gone.” If this were done, the fund is so short of money, it wouldl go broke in 10 years, . . . leaving nothing for anyone after that.

Ref: The Kansas City Star

This is the sort of thing that happens when pension funds fail to collect sufficient contributions, . . . as many private, state, and federal funds do, . . .

and interest rates fall to near-zero% as a direct result of Federal Central Bank policy.

DonDiego suspects many other pension funds will soon find themselves in similar financial peril.

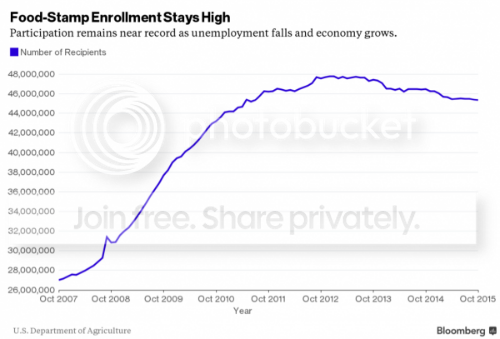

One might reasonably expect the enrollment in Food Stamps to rise eventually as a result.

Or one might just shrug one's shoulders and suggest there's nothin' to see here, . . . and just move along, . . .