Quote

Originally posted by: pjstrohQuote

Originally posted by: DonDiego

new, improved plans which likely offer higher premiums, higher deductibles, and less choice in physicians, medical facilities, and pharmaceuticals.

Today's LVA vocabulary lesson:

Likely (adj) 1. such as well might happen or be true; probable

2. belonging to 3% of the US populatuon

Is pjstroh willing to say

anything to try to make Obamacare look good?

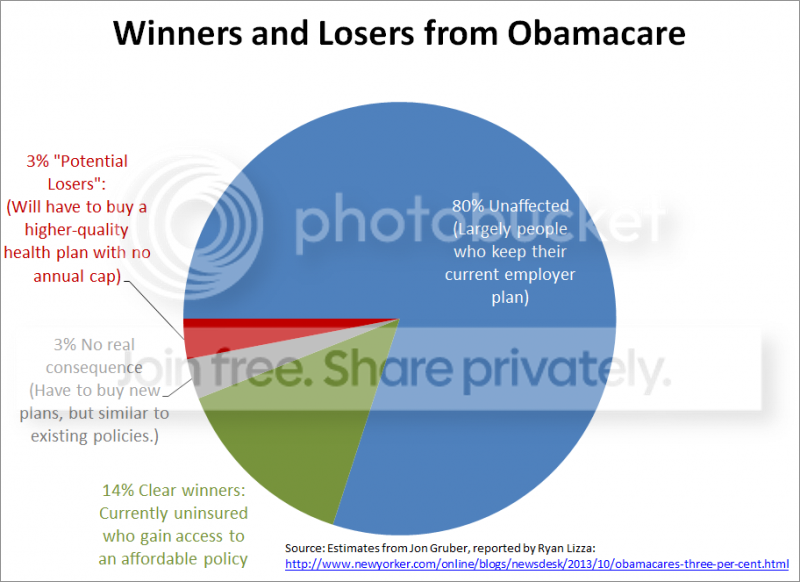

The reason 80% are unaffected is because they are covered by employer-provided insurance which is not subject to Obamacare

yet. Next year, . . . purely by coincidence

two months after the mid-term elections, . . .Obamacare will apply to employer plans.

Perhaps, . . . just maybe, . . . the current debacle and revelations therefrom will result in this whole farce being reversed somehow. But if not, what is happening to individual healthcare plans now will repeat itself on employer-provided group plans.

DonDiego has already stated there are winners and losers under Obamacare.

One problem is the Government is choosing the winners and losers, . . .

i.e. as usual, the scheme is employed as yet another redistribution of income. For the record, the Government

never chooses DonDiego as a winner.

But the worst aspect is the lies employed by those who proposed Obamacare, passed the legislation, and now administer and defend Obamacare. The promises were costs would be lower, citizens would be allowed to keep their insurance, citizens would be allowed to keep their doctors, etc.

And it would be cheaper.

These were all lies. And the Government documents reveal the folks implementing Obamacare knew they were lies.

There are costs involved with covering more people. There are costs involved with covering pre-existing conditions. [By definition covering pre-existing conditions means Obamacare is not insurance.] There are costs involved with requiring everyone to pay for standard policies which include certain insurance which they do not require,

e.g. pediatric care for 60-year-olds.

The insurers have raised prices to cover these costs.

And for the same reasons next year Obamacare will be more expensive and limiting for the "80% unaffected"; DonDiego supposes many of the "80% unaffected" will not be pleased.

If things work as the planners planned Obamacare will be more expensive overall than the prior condition.

And if younger folks are rational many will choose to pay the penalty-tax instead of joining Obamacare. Then the premiums to pay for Obamacare will be insufficient and the insurers will raise prices next year.

And in the event Obamacare survives for three more years the penalty-tax rises to 2.5% of one's income. At this point DonDiego expects the younger citizenry to take to the streets seeking redress. If the ObamaDrone Fleet is operational, DonDiego expects this rebellion to be put down rather quickly.

Maybe this was all part of the original plan from the beginning.

* * * * * * * * * * * * * *

Oh, . . . by the way, . . . DonDiego was curious why the lower portion of the otherwise helpful chart cited by pjstroh and forkushV was, . . . umm, . . . missing, . . . probably inadvertently.

So he found it, . . . on the internets:

DonDiego did not find the chart at the link indicated on the chart; he could not see it, as it was missing, probably inadvertently, from the chart as posted by pjstroh and forkushV.

When he

did find the chart, he discovered he could not link to the address anyway; "the content is no longer available". Why? Ah well, . . . things happen.

Luckily the website on which DonDiego found the chart, Business Insider, includes a critique.

Some critiques:

__The 14% "clear winners" is likely more like 8% or less depending on, for example, how many choose to pay the penalty-tax. Many of this 14% will remain uninsured.

__The 3% "no real consequence" actually contains winners and losers. [Costs will rise.-DD]

__The 3% "potential losers" actually contains winners and losers. [Incidentally, defining an Obamacare Plan as "higher quality" on the chart does not mean it

is higher quality for the insurance purchaser.-DD]

This leads to DonDiego's fundamental question:

"If the problem was the 14% (or maybe only 8%) uninsured citizens, why was the solution a complete change to the entire health insurance industry in the United States - including loss of access to medical facilities, loss of access to preferred medical doctors, and higher costs overall to those who were insured?"

Oh, . . . wait a second, . . . is that a drone DonDiego hears in the distance?