Quote

Originally posted by: Boilerman

Forkie, it's quite apparent that Nick's quote was accurate and true.

Originally posted by: Boilerman

Forkie, it's quite apparent that Nick's quote was accurate and true.

Not really.

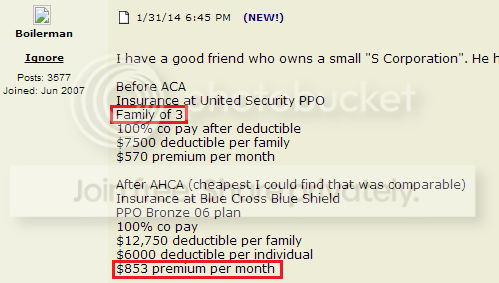

Nick and his family of nonsmokers, aged (53, 52, and 19) can get their bronze Obamacare coverage from Blue Cross/Blue Shield of Illinois for a couple hundred bucks less than the $853 a month you claimed:

This is far superior insurance to the short term plan that Nick apparently had last year. This bronze Obamacare plan from BCBS is different from Nick's old plan in that it:

* is available to people with pre-existing conditions;

* doesn't have lifetime caps;

* doesn't exclude kids when they turn 19;

* includes preventative care;

* is renewable; and

* doesn't allow the insurer to cancel the policy a month after someone in the family gets sick.

In the end, it's not really important which policy Nick chooses. But there's can be no debate that Obamacare is delivering to Nick and his family far superior coverage for less money ($549 vs. $570) than his old plan did.

So what was your point in brining up Nick again? You wanted to illustrate another person benefitting from the law? Well done!

Nick and his family of nonsmokers, aged (53, 52, and 19) can get their bronze Obamacare coverage from Blue Cross/Blue Shield of Illinois for a couple hundred bucks less than the $853 a month you claimed:

This is far superior insurance to the short term plan that Nick apparently had last year. This bronze Obamacare plan from BCBS is different from Nick's old plan in that it:

* is available to people with pre-existing conditions;

* doesn't have lifetime caps;

* doesn't exclude kids when they turn 19;

* includes preventative care;

* is renewable; and

* doesn't allow the insurer to cancel the policy a month after someone in the family gets sick.

In the end, it's not really important which policy Nick chooses. But there's can be no debate that Obamacare is delivering to Nick and his family far superior coverage for less money ($549 vs. $570) than his old plan did.

So what was your point in brining up Nick again? You wanted to illustrate another person benefitting from the law? Well done!